Interest rates increased after almost a decade

So Finally FOMC increased the interest rates this week by .25% after almost a decade as expected. Though it was fixed since 2008 at 3.25%, June 2006 was the last time it was increased.

Federal Open Market Committee (FOMC) mandate is to determine the prime interest rate & money supply.It was formed through the Banking Act of 1933 & were supposed to meet four times a year. However since 1981, they are meeting every five to eight weeks at least 8 times a year to fulfill the same mandate.

Increase in interest rate indicates confidence in the economy by the Feds. Although they would be aiming for much higher increase, this increase would be a litmus test to see how far can they stretch. Higher interest rate means it is expensive to borrow money driving valuations of assets down. For a common man, increased mortgage rate makes it less affordable to own a house.

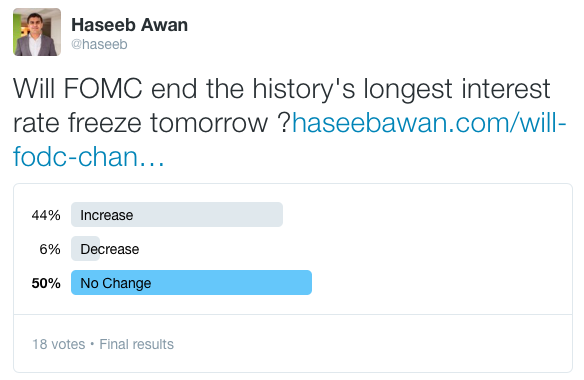

This increase in interest rate was expected and overdue. A twitter survey indicated mixed result as below.

Increase in interest rate will strengthen the dollar because it attracts more investment in the country. Investors can earn more money by keeping their money in saving accounts in US and demand of US dollar goes up. Interest rates are still very low. Just as a comparison it was 21.5% on December 19th 1980. Following is the graph of interest rates since 1947.

We are living in economy of 3.25 prime rate for the last 7 years. Higher interest & dollar rate have negative impact on international loan-burdened economies . They are already struggling with repayment of loans & now they have to pay even more. On the flip side, it will make it difficult for US vendors to sell internationally because their product have became more expensive and the competing products from other countries have became cheaper. At the moment, effects would be minimal but it would be interesting to watch out for their next meeting on January 27 & 28.

Looking forward to post 3.5% economy.