Haseeb Awan is a Financial Technology (FinTech) entrepreneur with a track record of two successful business exits, raising over 100M in venture capital & growing the customer base from 0-4 Million users & expanding to 15 countries across 4 continents within 18 months. He has been included among the top 100 influential people in FinTech globally, won multiple international awards, wrote for and is mentioned on multiple international media & frequently speaks at international conferences & government committees. He is Engineer by degree with Master’s in Engineering Management & also has studied Financial Markets from Yale University & holds Project Management Professional (PMP) designation. He is also a Y-Combinator Alumni as well Next Founders & couple of other associations. He is among the earliest entrepreneurs in blockchain space & personal investor in 30+ companies & advisor to over 10 companies.

Bitcoin is considered to be too sacred when it comes to critisism in cryptocurrencies. Bitcoin minimalism has developed a cult culture where anything that comes remotely close to taking away the dominant position from bitcoins in cryptocurrency is hit with criticism. While I don’t disagree with the BTC dominance, it is hurting the growth of ecosystem. Altcoins also known as shit coins have diluted the space but they’ve a reason to exist.

My involved in the industry span over 7 years & have witness bitcoin narrative being sold shifting from transfer of value to store of value. Ethereum was at one time referred to as bitcoin 2.0 though the function & use case was totally different. As much as I love bitcoin, matter of fact is that bitcoin wont’ work with security tokens & there has to be a different chain to accommodate this use case.

Here are few of the reasons why Security tokens have a different trajectory from bitcoins.

Decentralization

Bitcoin is decentralized & there isn’t any restriction on who can own, transfer or mine bitcoin. There is absolutely no KYC or filter to censor any one. With STs, there is a set of regulation that gets tagged along & impossible to be imposed with bitcoins. If some thing can’t be audited & controlled, it won’t fly with regulations.

Perception Issues

Bitcoin till date have kind

of stigma attached to that which has refrained multiple brand names and status

quo to stay away due to additional risk that may have a bad reward/risk ratio in

their books. For STs, blockchain should

come clean with no prior baggage

Non-Recoverable

There is a sizeable quantity of bitcoin that are lost forever due to one reason or another. Similarly there has been incidents of hack or private keys loss. In traditional world, if you lose your certificate you can get a duplicate, but in blockchain if it’s gone once, it’s gone forever. STs must have a mechanism to reverse & fix these transactions

Limited Functionality

Reason why Bitcoin is now

referred to as storage of value is due to limited functionality. There is very

little which you can do with your bitcoins. Yes there has been forks to improve

some of the desired features or sidechains, but overall it’s like running a

bullet train on existing track. You’re losing efficiency. STs need creative functionalities which will

need an entirely new chain

Lack of KYC

With STs every stakeholder

is identified, and this process is enforced. With BTC that’s not possible and there

isn’t any discrimination between any of the participants.

This list isn’t exhaustive

but just gives a rough overview why there would be a new chain(s) that will

serve the next layer of Security tokens. Once this has been realized among the

industry, there would be more R&D into developing those protocols.

While

general consensus about ICO is that the days of ICO (Initial Coin Offering) are

over post 2018 crash, IEO (Initial Exchange Offering) is generating similar

kind of buzz wave. I can see lot of co-relation

between ICO & IEO when it comes to FOMO, interest, price manipulation etc.

Major difference between IEO & ICO is IEO is supported by an exchange while

ICO has to get listed on an exchange. Due to ICOs performing really bad in 2018

mainly due to lack of liquidity IEO does covers that portion rally well. While there

are only handful IEOs executed, results are very encouraging for initial buyers

with returns resonating to ICOs in early days. I expect it to follow the same

hype cycle of ICOs but on a relatively smaller scale.

Let’s

cover this more in detail.

What

is an IEO?

Initial

exchange offering is administered or conducted on the platform of a digital

exchange also called cryptocurrency exchange on behalf of the startup that

looks for funds for its newly issued tokens.

While

ICOs generally use their own website or 3rd party tools to conduct the

token sale process which isn’t link to exchange. Post-sale, exchanges get involved

where they determine if they want to list the token or not. Through IEO, exchange

listing risk is mitigated.

This

facilitation however come with a price tag which is either a fix fee or percentage

or combination of both depending on the arrangement between token issuer &

exchange they’re using. Generally the fee structure varies from 50k USD to 500k

in fixcost plus 5-10% of the total sale.

With

struggling exchange business, this can provide much relief to their operations

if done correctly however they won’t like to conduct lot of them to keep the

scarcity.

How

are IEO and ICO different?

While

I’ve mentioned the major difference between ICO & IEO, here are the fine prints

In case of ICO, fundraising is conducted at the

token issuer’s website while IEO makes use of the platform of the digital

exchange that conducts the token sale.

The crowd sale counterparty for ICO is the

project developer but in IEO, it is the cryptocurrency exchange.

The smart contract is managed by the company or

startup conducting the token sale for ICO and in case of IEO; it is the cryptocurrency

exchange that manages the smart contract.

In ICOs, the marketing budget needed by

fundraising companies is significantly high. The project would have to invest

many resources to get the attention of the public and investors. In Initial

Exchange Offering, the marketing budget is relatively low as the exchange

actively markets the tokens of the startup.

There is no screening required before a startup

can launch an ICO but is required in IEO and the exchange screen the company

before it allows it to fundraise on its platform.

Another difference is that only after the

funding gets completed, ICOs mint their token while tokens are generated by the

project and sent to the exchange platform in case of IEO.

IEO promises higher Liquidity, transparency and

protection than does ICO.

Vested interest of exchange provide some level of oversight over the project.

Liquidity

crisis for ICOs

“When Binance?”is possibly

one of the most asked question in telegram channels because investors are

looking to offload their purchased tokens for multiple returns and moving onto

the next one. As if running the project itself isn’t a hard task, exchange

listing consumes both human & financial capital.

Creating a token is super

simple but listing it is super hard specially on big exchanges. Though there

are probably more than 300 exchanges globally, 1% of them own 90% of the volume

& that’s where the competition comes in. Not just that exchanges are

charging for exchange listing fee, the volume need to be significant else there

is a danger that the token will be delisted. To avoid that firms do pay up for

market making, which isn’t just ethically & legally questionable but also

financially expensive. Orphan tokens end up in decentralized exchange or tier 3rd exchanges where volume is close to nothing. As per few reports only 1 out of 5 tokens

was able to be listed. Number for tier 1 exchange is probably 1 out of 15.

It cost anywhere from $100,000 for tier 2/3 to $3M

for tier 1. There has been claims of charging $5M – $8M during the bull markets

as well. Exchange rather than specifying it as listing fee, they call it due diligence

cost. In all honesty, they’ve to perform the due diligence because they can get

into trouble by offering something that could be fraudulent.

State of IEO:

The

first ever cryptocurrency exchange that embraced IEO was Binance and launched

its IEO platform Binance Launchpad. BitTorrent (now bought by TRON) conducted a

token sale on Binance Launchpad in January and raised $7.2 million in a short

span of 15 minutes & generated 4X returns within days . Fetch.AI was the

second IEO on the same platform that hit a hard cap of about $6 million in 22

seconds. The Binance Launchpad was a success and how could other exchanges miss

out such a lucrative opportunity (they charge listing price and a percent of

the fund raised) as they started launching their own IEO platforms.

The

Singapore based major exchange Huobi jumped into the ring by launching its own

IEX platform. However, to look different from its competitors and to attract

more investors, they named their fundraising model DPO Direct Premium Offering

and is prominent for allowing users purchase crypto at a price lower than the

market price. KuCoin wanted to “reveal the hidden blockchain gem” and launched

their KuCpon Spotlight. The Malta Based exchange OKEx announced about the

launching of their platform OKJumpstart for holding IEOs on March 13. Bittrex

IEO is an upcoming IEOs scheduled to be launched in the first week of April.

ICO

vs. IEO. Which one is preferred?

Back

in July 2013, Mastercoin held the first ever ICO initial coin offering which

was vigorously followed by many Blockchain projects fundraising in the same way

however ICOs have many flaws slowing down the progress of fundraising and this

engendered the need for other means of fundraising like STOs Security Token

Offerings and now IEOs which has actually created a buzz in the crypto world.

Some

people might argue that IEO is the same old wine in a new labeled bottle but

that is not true. Though both IEOs and ICOs share the same rationales of IPOs

Initial Public Offerings, both are fundamentally different. What makes IEO

unique is that the project has to pass through a comprehensive assessment by

the exchanges in order to curb problems face by ICOs-Scams. This way, IEO

becomes riskless for investors to put in their money unlike what the scenario

had been during the ICOs craze when investors would invest in any ICO including

those who could offer even a white paper. This is the reason why majority of crypto

experts prefer IEO over ICO.

The case

of RAID IEO is a best example here. Bittrex had recently cancelled the IEO for

RAID project just hours before the start of token sale. The reason behind why Bittrex

cancelled IEO for RAID was the termination of partnership between the e-gaming data

analytics platform OP.GG and RAID. Bittrex considered the partnership between

the companies an important part of the project and the termination of the

partnership simply made the token sale redundant and not in the interest of the

consumers of Bittrex.

Major

Advantages of IEO

The

biggest advantage of IEO for the team/project is quick access to vetted

investors and hence funds just like the companies that after launching their

IPO initial public offerings get their name listed on NASDAQ exchange and get

access to funds. Couple of days ago I read in an autonomous research that ICO issuers

have no other option but to pay an amount anywhere from $1 million to $3

million to get their tokens listed on an exchange. Further adding, there are

additional costs as well like they have to spend on running marketing campaigns

and hiring advisors. Since exchanges still charge high listing fees and share

in the funds raised for conducting IEO, the startup/team behind the token get

time to focus on the project development and not on marketing and fundraising.

It

is an open secret that exchanges earn a lucrative amount of money in the form

of listing fee and share in the funds raise which further depend on the size of

the platform. In addition, IEO participants after creating an account on a

particular exchange might still roam around and ultimately become regular

costumers.

Finally

investors who participate in IEOs face the least risk. They simply create an

account on an exchange and can participate and purchase tokens in any IEO launched

on the exchange instead of creating many accounts and dealing with a number of

wallets on different exchanges. Leading exchanges such as Binance make sure the

projects pass a vetted process of assessment before the token sale gets

conducted on the exchange because they do not want to loose costumers by

getting their reputation spoiled by cooperating with an illicit or fraudulent

project which means there is always a higher degree of trust in case of IEO. However,

in case of ICOs, you could be at risk if you are not good with spotting scams

and dubious projects. A legitimate exchange will never host scams so if you are

a member with one, you would face the least risk. Initial Exchange Offerings

IEOs allow investors to take part in Initial Coin Offerings ICOs with low risk.

Challenges

for IEO

Non-compete between exchanges

When a token is launched independently

there isn’t any affiliation with a specific exchange so it can be listed on

multiple exchanges exposing itself to lot of users. My concern is that if a

token was sold through a specific exchange there may be reluctance for other exchanges

to list it specially the competition one. While goal of crypto is to build an

open financial system, this may lead to a silo approach.

Lack of volume

While IEO does guarantees exchange

listing, it doesn’t guarantee a volume. If the volume drops a lot, there is a delisting

risk.

Regulatory risk

While they’re

marketed as utility tokens, there is a chance that they’re a security in

multiple jurisdiction. In that case they would have be classified under Security

Tokens, which I’ve covered in detail here.

Delayed liquidity

While there is a guarantee that

it’ll be listed on exchange, the firm offering the token may delay listing due

to any factor. Major factor would be product not being ready or bear market.

Lack of lock-up period

In case of traditional IPOs,

there is generally a lockup period for early investor but so far there isn’t

anything like this in IEO. This can

create a pump & dump scheme, so buyers beware & don’t buy into any

hype.

How

to become an IEO participant?

You

need to follow five steps to take part in IEO.

Throughout the last year,

the fame of ICO has dwindles to great extent but they still are the main mediums

for fundraising for many cryptocurrency projects. So first of all you need

to be sure if an IEO is going to take place by checking the website of the

startup/development team.

You need to know about the

exchange that will conduct the IEO. If you are already registered on the

exchange and have a wallet, you move on to the next step. If not, you need

to create an account on the exchange in order to participate in IEO

because a token issuer may sign an agreement with only one out of many

exchanges and in that case, you would have no other option but to create

an account on the exchange.

You need to complete your

KYC Know Your Costumer which is an anti money laundering AML procedure.

Once you are registered with an exchange, you would have to go through a

sought of verification procedure to reduce security risks. You need to do

it as soon as possible because it may take the exchange some time to get

your identity confirmed.

Now you need to find out

the crypto option that is available. You normally have the options for ETH

Ethereum and BTC Bitcoin over the exchanges except for some in the likes

of Binance who go with their own tokens.

Finally, you need to wait

for the time until your Initial Exchange Offering IEO starts. Make sure

you are present minded and do not miss the token sale for it might only

last for couple of minutes or may be less (the case of Fetch.AI).

IEO!

The next fundraising boom?

Back in 2017 & 2018, ICO engendered a fundraising boom

in the crypto space but a notable number of ICOs were conducted by scammers,

looted investors who blindly trusted every ICO and this was the sole reason why

ICOs lost their glory and prestige. In addition to ICOs with dubious nature,

ban on ICOs in countries like China, Macedonia, Nepal and Ecuador exempted a

big source of funding for the startup and companies who wanted to fundraise for

their tokens. Since IEO ensures provision of high level trust, security,

project credibility and instant fundraising, it is no doubt going to engender

the next fundraising boom in the crypto space and hence will become the

standard model for raising funds.

Conclusion:

Having

said that, one might argue that there is nothing like a perfect crowdfunding

model/mechanism because since Mastercoin till the present day IEO, we have been

seeing so many crowdfunding mechanisms with ICO the most prominent among all but

due to the arrival of IEO, even ICO looks in hot water. Things can change. We

have seen things getting flipped 180 in matter of days. Who knows about the

future? The life span of IEO could be shorter than that of ICO as well. It

depends on how advanced the new crowdfunding mechanism is. A more advanced CFM

than IEO will no doubt dwindle the prospect of survival of IEO. But for now, the

perks and benefits promised by IEOs are way too lucrative to be ignored and as

a result, it will take priority over ICO but I still think STOs are the way to

go for any similar offering.

The velocity of an object is the rate of change of its position with respect to a frame of reference and is a function of time. Simple example is car travelling at 100 mph. Though it’s a concept of kinematics, relevance can be derived in economics and more specifically in tokenomics.

In tokenomics, price of token is directly linked to usage. However, usage isn’t the only metric & this is where velocity comes into play. Gyms operate on a 100X principal to be profitable. They’re looking to get 100 times memberships than the capacity because they know not everyone is going to show up at same time, but if they do they’ll in trouble. What if a single membership is valid for 1 person at any given time & people can share it. This will lead to 99% drop in their memberships collapsing their 100X model.

Basic premise with respect of membership is that it’s linked to an individual person vs individual usage & isn’t transferable. In case of tokens, this model does have a flaw because they’re so easy to transfer. Take an example of gym where a company issued 1000 tokens for a gym with a capacity of 10 people. Now there is an intermediately company which bought 10 tokens & setup a rent-seeking program where users can rent whenever it’s needed. In this case, gym business has been screwed. None of the users have incentive to hold membership because they can borrow it whenever they want.

This is where the concept of token velocity comes. Since the basic promise behind holding a token is that you get something in return. Now the question is whether these returns are perpetual or one time. If it’s one time, then there isn’t any incentive for the owners of the tokens to hold them but if they can be flexed over time, they would have incentives to hold them as long as they see the benefit.

Similar to automotive mph term, here it’s uot which stands for “usage over time”. More usage in a short span of time leads to higher demand & lower usage over the same time would lead to lower demand. Usage is directly correlated to demand & result into price changes.

One Time Returns could be:

– Accepting cryptocurrencies to facilitate customers or attracting a new set of customers. Seller don’t have to hold it because the benefit has been reaped & is one time only

– Accessing a network to perform a single usage action without preserving your history. Example would be buying a concert ticker which is one-time event. You may attend other concerts but there would absolutely no correlation between both of them

– Proof of Work (PoW) tokens, miners can immediately sell it because the output has been achieved

– Transfer of value where a company requires a payment in specific token and you only purchase it for that specific payment.

Perpetual Returns:

– Stake in decisions that you’re passionate about. More like a voting power. Example would be uber drivers earning tokens & have a say in the company policies based on how many rides he has completed and similar rights for the riders.

– Right to participate in a network without transfer privileges. Example is having a membership to a club where you can’t transfer your membership. If you decide to give it up, it’s burned and never available again.

– Identity management in the network. You may use Facebook once a day however you want to preserve who you’re & despite the concert example given above your identity does matters

– Novelty or exclusivity where there are only a specific number of people allowed into the network. Once it’s closed, you can’t participate anymore.

– Pedigree building where companies incentivize long term holders. More like a loyalty give away. So, if you’ve a token of a movie theatre for 5 years, you’re allowed to book the best seat

– Profit Sharing. If the network is growing and sharing the economic upside with the token holders, they’ll hold the tokens to reap the benefit. It’s similar to dividend paying stocks

– Price appreciation. If there is an economic upside with holding tokens that’s based on fundamentals, users would like to hold the tokens. All praise to the rising sun however it does lead to plateau or crash after a while if the fundamentals aren’t there.

– Secondary benefits such as discount at a restaurant if you hold a specific gym membership

– Discounted network spent where if you earn tokens within the network & spend it back into the network, you get a discount. Example would be Airbnb allowing host to get 100% off on the fees AirBnb charges if you spend you don’t withdraw your earning.

– Discount on company products if you’re holding their tokens. So if you’re amazon token holder, you get 50% discount on the profit that amazon makes off that sale

Summary:

Since tokens do allow frictionless transfers, they would come up with schemes to reduce token velocity. With higher token velocity, they’ll struggle with building an ecosystem and it’ll have a negative impact on their pricing. It’s the network strength & demand that can allow them to decrease token velocity. Ultimately if a token is so strong that it does start acting as an asset class that’s where the companies will be able to grow exponentially. Companies will have to look into the velocity problems to encourage long term holders for non-speculative reasons.

A securities offering (or funding round or investment round) is a discrete round of investment, by which a business or other enterprise raises money to fund operations, expansion, a capital project, an acquisition, or some other business purpose. A securities offering (or funding round or investment round) is a discrete round of investment, by which a business or other enterprise raises money to fund operations, expansion, a capital project, an acquisition, or some other business purpose.

STOs

would be a process to move traditional assets to blockchain & evolving the

way assets are issued, traded, held & transferred. It’s a work in progress

with blocks built around it to support the ecosystem.

There are many steps involved in security tokens but here are the 6 basic ones

1 – Asset

First step to find out the asset that you want to tokenize.

They could be anything from gold to equity to real estate. For sake of ease, I’ll

use the Real estate example since that’s the most lucrative asset class that can

be used in STOs. There is an economy of scale that isn’t available to retail

investors plus it’s considered to be the safest among majority. Results are not

the greatest but significantly low risk/reward along with the perception of

physical asset makes it the favourite.

Real estate is a 265 Trillion dollar asset class & only 1% of it is semi-liquid or available to retail investor through complex REIT structures

2 -Prospective

It’s combination of pitch deck & business plan. Once you’ve finalized an asset, you’ve to put down all the pros/cons, risks & rewards on paper. Make sure you’ve kept a contingency & buffer in all your calculations. Rewards always is late since things always cost more & take more time. Be super conservative while putting together the numbers. If you’re able to pull off better results, you’ll make your investors happier but if you’re not able to perform, you’ll have many unhappy customers. As they always say “under promise & over-deliver”. While you may have in-house capabilities, it’s very important to have an independent outside assessment of the project. Brand name accounting or valuations firms are expensive, but they’re well known & does add a high degree of trust in the offering.

3 – Technical

While Blockchain may looks like an alien term to many, it’s fairly easy to launch an STO from technical stand point. It’s almost like setting up an email account. You would need basic information & token platforms have written extensive guides on it. I’ll compare token platforms in a separate blog post. It would be good idea to connect with each of them & assess them. It shouldn’t take you more than 3-4 days in this step. Just make sure you’re credentials are protected

4 – Legal

This part should be taken super seriously since you can land

into lot of trouble by not having proper legal advice on your offering. Security

offering is overseen by multiple regularity bodies but the most important is Security

Exchange Commision ( SEC). Ontario Security Commision ( OSC ) oversees activities

involved in Ontario. There are similar organization in every jurisdiction.

While offering Security tokens, you’re not just limited to your incorporation jurisdiction

but also the investor or even the asset existance. Example is you’re a Canadian

Citizen tokenizing a building in Sydney while you’re firm is incorporated in

Singapore & your investor is an American Citizen based in Barbados. Now you’ve

to make sure you’re not breaching terms of either of the jurisdictions, in this

case Canada, US, Australia, Barbados or Sydney. To simplify it, you’ve to set a

high bar for participants & a good security lawyer would be able to guide

you through. Keep around 30-45 days for this step.

Here are couple of things that you would’ve to deal with while

launching an STOs

Determine the best structure for the STO

Review & draft the rights, dividends language used

Preparing a compliant private placement memorandum ( PPM)

Preparing a purchase agreement for the buyers

Investor qualification questionnaire involving KYC/AML & accreditation process if required by the offering

Filing the report with the SEC or respective regularity authority

5- Marketing

Now you’ve to get people interested in your STOs. While you

want to be aggressive in reaching out to as many people as possible, you may be

limited by who you can offer this because of the accreditation limits imposed

by SEC.

Here are the accreditation requirements

An annual income of over $200,000 individually,

or $300,000 with a spouse, maintained over the previous two years and with the

same expectation for the current year.

Net assets worth upwards of $1 million, excluding

the primary residence (unless more is owed on the mortgage than the residence

is worth).

An institution with over $5 million in assets —

e.g. a venture fund or trust.

An entity made up entirely of accredited

investors.

Recently few liberal policies have been

introduced to allow non-accredited investors to participate, but it does have its

own limitations. Transparency should be the top priority & there isn’t

anything like limited information.

Investors are generally lazy & for REITS

they’re fairly conservative. Your marketing plan should be so clear, concise that

it doesn’t requires a PhD in finance to understand it. Provide as clear &

concise information as possible. I’ll share some templates on building a good

prospective, but here is a good guideline on what to include

Legal disclaimers and any other key legal notices

The details of your product

An overview of the industry you operate in

The architecture of your product (technical)

The model of your business and your structure

How you intend to market your solution

What your Tokens are backed by, including any other forms of security that are applicable

Details on how the Token can be used and the economics behind it

The members of your team and who your technical advisors are

6 – Fund raising

Once you’ve the marketing plan ready, you’re now ready to launch. While it probably be an online process, you should’ve built a momentum offline. There is nothing worse that launching an offering with 0 contributors. Good rule is to have at-least 25% capital committed before hand. Once you’ve launched it, there should be an influx of early contributors to build the momentum. More tips on this specific topic in upcoming blog posts. It’s very important to have a way for investors to ask questions. You can host webinars or Ask Me Anything (AMA) sessions. In case of ICOs companies were keeping a full time community manager to manage social media & messaging apps, but that may be excessive in case of STOs.

Do’s

Be transparent, conservative, concise &

compliant

Over communicate with the buyers.

KYC/AML check on your buyer

3rd party audit of your offering

Don’t

Use vague language,

Provide assurance of guaranteed result

Offer a high risk/reward ratio product

Solicit investment from non-accredited investor unless you’ve

security clearance

Sell without legal preparation

Conclusion

I hope this’ll post would’ve

helped you in getting ideas on process required to launch an STO. This guide

isn’t extensive, but I am launching a podcast & book that would entail lot

of information. Subscribe on my website to be informed when it does launch.

While the entire process looks fairly complicated, I am happy to give my feedback or chat about your ideas. Use the link below to contact me.

5 years ago, we installed the first bitcoin ATM in Toronto at Decentral. These 5 years passed by quickly. I am humbled by the people I met, experiences I had & opportunities I got through that experiment.

That venture started as a fun weekend project that turned into a business. Today it’s a thriving company. I’ll cover that story later but today I’ll write about why I think Bitcoin ATM is a killer use case for cryptocurrencies.

It’s fairly easy to buy bitcoins in today’s age & date however it wasn’t the situation in 2013. We had disasters like MTGox in addition to some shaddy exchanges which wanted you to transfer funds to an offshore entity. At time it used to take months before you can see your money in bank account. Bank accounts were also getting shut down for just dealing with an exchange.

Idea behind Bitcoin ATM was very simple. It’s a simple machine that converts fiat into bitcoins & vice versa. It was considered one of the most unpopular startups due to it’s nature. Like here everyone is building next generational cryptographic solutions & here we were cranking steel boxes with cash recyclers. In the utopia world of crypto, it was hard to make an impression & was laughed upon.

5 years passed by & today there are over 4,000 BTMs serving performing millions of transactions every year. For majority of people, their first interaction with bitcoin was through Bitcoin ATM. I do often come across stories of how people use these machines. It’s one of the most important component of the entire cryptographic currency movement.

I still to date believe that one of the most weakest link in the decentralized financial world is traditional banking. Today if banks shut down any exchange bank account, they’re done. Building an exchange using a bank is like building an AirBnB in the lobby of Marriot

Here are some interesting use cases around how these Bitcon ATMs can do more than just

Bank Account

People can buy stable coins through it & store it in their wallet. Banks are generally only interested in banking the top 1% so there is a big number that can be served.

Infrastructure as a Service

These BTMs can be used to offer services to unbanked directly from these machines. Companies can built applications targeting this market segment & BTM can serve as an intermediary

Money Transfer

Despite digitisation majority of the money remittance is done in cash. 80% of the expenses for a money transmission company are due to location & KYC. BTM can slash these expenses by 95%

If you look at any financial institute, they’ve to dependent on SWIFT or central bank network for transfer of fund. Through BTMs foundation of an independent financial system that be laid which can be built parallel to legacy. This system have it’s own rail tracks allowing more flexibility. There is a bigger opportunity to build a network of BTMs which can perform any function that any other financial institute can perform.

These BTMs can have cash recycler and in an ideal scenario there isn’t any need to replenish or fill up the cash. They can independently operate & replace any branch effectively improving profitability 5X.

Have you ever used a Bitcoin ATM or is there a Bitcoin ATM nearby yours ? Also what else do you think these BTMs can do ?

Financial cycles are often misunderstood by majority. It’s a zero sum game where transfer of money takes place from one entity to another. It’s combination of analysis, research but luck outplays every other factor. Markets react irrationally majority of the times.

Either you’re a fund manager or an individual managing your personal portfolio, what’t the #1 question that goes through your mind.

“Is this a great time to exit or enter”

There are three types of sentiments that exist in the market at any given point of time.

Market Neutral

Bullish

Bearish

Every one in the market has a conviction behind his decision once he is able to identify the trends based on the information he has. General trend is to follow the trend and don’t ride against the wave, however if you look at history biggest gains are made when people went against what market was doing.

Quote from 2004 Annual Shareholder Letter for Berkshire Ha

Warren in the letter explained how well the stock markets have performed & index funds was the best investment that people could’ve made, but he outlined the 3 biggest traps for any investor

Trading too much & incurring fees

No or little stock analysis

Poor skills at timing the market

He also mentions that though these are the obvious ingredients for failure, they’re added to the receipt of success repeatedly

Gold mines are found when you’re patient and have your own strategy. I’ll cover the following

Why is it a good idea to go against the market

Why crashes always follow bubbles

Why risk-free is actually the most riskiest approach

Before I dive into more details, let’s start with the basic notion behind investor mentality. He is always looking for one thing

Buy assets with high value at a low value. Delta between actual value & value he paid is the profit

My job is to invest in a wide variety of assets & construct a portfolio with different strategies to yield results beating the market average. History suggest than less than 33% of the people are able to beat the market average, but the returns for 33% are so high which keeps the remaining 67% in the game. Luckily, I am among the 33% so far, but I could be on other side of the table anytime.

Luck plays an important role in any investment outcome regardless of how much research one has done. Some are better at guessing by chance or by research, but no one has a crystal ball to predict accurately. Best thing an investor can do is to construct a thesis around a hypothesis, build a strategy around it with a backup plan & then discipline himself in following it. Every failure or success should take him back to the working sheet to validate or invalidate his assumptions.

While research is good, the biggest factors involving the market cycles are large-scale economical, geopolitical or market-related events including but not limited to security, war, military take-overs, political instability, natural resources discovery, big trade agreements or a technological breakthroughs. With advent of internet, every one has access to this information & now it’s up-to their intellectual ability to absorb, assess and guesstimate the impact on the markets.

There are multiple types of traders. It could either be day-trader, long term investors or just wicks scalper. Regardless of whoever you are, it’s the exact same mission. Beat the market with your decision. You can either be investing in hope of price increase, generating cash flow or just diversifying your asset to preserve capital, but every move you determine is nothing but just a speculation. Everyone is hoping to be smarter than others, but that rarely happens.

In the past, I acquired assets which were a steal but also picked up garbage that still to date I can’t believe. Biggest jackpot is when you’re able to time well. It’s like striking the ball in the right direction from middle of the bat. It’s super hard to time it well, so best is to have an exit and entry price & not worry about over optimising your gain. Just minimize your losses.

So what’s a cycle? They’re similar to any wave that you see at the ocean which comes and go however waves can be bigger or smaller. Despite their unpredictability, if you look at a longer time frame, you can have some level of confidence of the future. Example is night comes after day, but the time sun rises and set changes from season to season. We may or may not have a White Christmas in Toronto, but ruling out snow in January/February is very hard.

It’s easier to be right in the longer time frame while very difficult to be right in a short time frame. Reward to be right in a shorter time frame is higher but Risk reward ratio just doesn’t justify the action.

Today we’re fortunate enough to have access to so much information that we can plan our day very concretely. Though we don’t know if it’ll snow on 25th December, but history shows that there isn’t any January without any snowfall.

While it becomes super hard to predict a specific trend during the day, long term cycles are fairly easy to identify. We were in the longest bull run in the history with every assets giving returns that were unprecedented in the history for the last 10 years. General public does exactly opposite to Buffet suggested. People will jump into an asset class when it has already reached the peak and will shy away from getting into an asset when it has bottomed out.

Bubble-Burst cycle keep on repeating rewarding the smart, lucky and patient people while taking it away from the people on the other side.

Focus on Long term:

“There are only patterns, patterns on top of patterns, patterns that affect other patterns. Patterns hidden by patterns. Patterns within patterns. If you watch close, history does nothing but repeat itself. What we call chaos is just patterns we haven’t recognized. What we call random is just patterns we can’t decipher. what we can’t understand we call nonsense. What we can’t read we call gibberish. There is no free will. There are no variables.” ― Chuck Palahniuk

If we look at the great depression, dot-com bubble, 2008 recession or any other similar event, there are many commonalities. Biggest one is the rate at which things are changing. Similar to body, economies or growth can’t rely on steroids for long. You can have a shot here and there but overall it should have merits. Back in 2013, I recall there were only 2-3 investment firms which remained in single digits till 2017 where every one wore the hat of Blockchain VC with reported number of more than 100 in 2017.

Mushroom group of these wanna be investors was toxic because companies were raising millions in seconds where they won’t have even be able to raise 10k from traditional industry. Result bubble burst and cryptocurrencies have lost 90% of it’s market cap. This isn’t the first time it has happened and probably won’t be the last one. These however does act as a filter for part-timers. I read on this topic here

While things generally do recover, it may take much longer in few cases. Though there is more VC invested today in startups than 2008 but the house ownership hasn’t returned to even closer to numbers of 2008.

Overall, with population growth economy has to grow and research shows the poverty levels are improving as well, so there isn’t a mystery behind achieving reasonable growth. Perseverance is the goal. As they say whatever that goes up must come down.

Biggest challange with the short term mentality is to understand investor psycology. Research shows that 90% of the decisions that we do are irrational. Very few people are disciplined and our spontaneous decisions make or break our lives. We have our own mood swings, good and bad days & in few extreme cases it’s more like a pendulum from unbounded euphoria & bottomless despair.

#1 reason for short term market mentality is those pendulum mood swings. It could be euphoria-driven greed that lead you to go all in or despair-driven fear that lead you to sell everything. Either people think this is once-in-a-lifetime opportunity or the world is going to end. Biggest mistake people make is when they convince themselves that this time will be different.

Even though your heart is saying that markets are irrational, you get in for a swing trade. It just take one person to panic and the stack of cards start to follow down creating a dominos effect. Fear of greed or fear or losing, both are dangerous.

Though it’s super easy to comment on it, when you’re in the moment, it’s very hard to resist even for the best of the best.

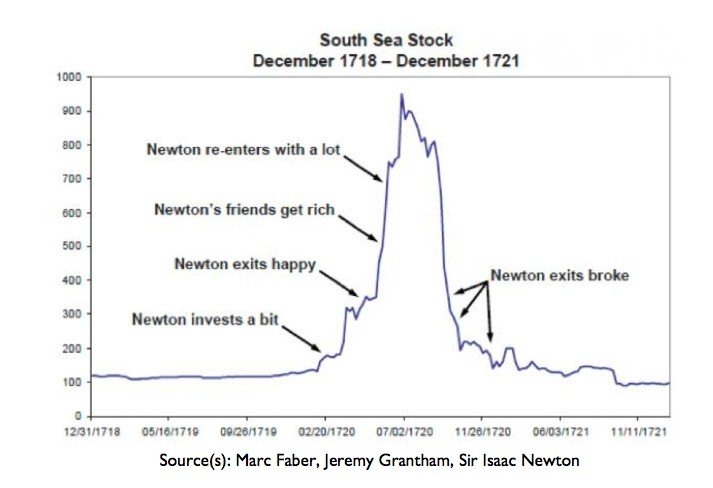

An early example is the case of Sir Isaac Newton and the South Sea Company, which was established in the early 18th Century and granted a monopoly on trade in the South Seas in exchange for assuming England’s war debt.

Investors warmed to the appeal of this monopoly and the company’s shares began their rise.

Britain’s most celebrated scientist was not immune to the monetary charms of the South Sea Company, and in early 1720 he profited handsomely from his stake. Having cashed in his chips, he then watched with some perturbation as stock in the company continued to rise.

In the words of Lord Overstone, no warning on earth can save people determined to grow suddenly rich.

Newton went on to repurchase a good deal more South Sea Company shares at more than three times the price of his original stake, and then proceeded to lose £20,000 (which, in 1720, amounted to almost all his life savings).

This prompted him to add, allegedly, that “I can calculate the movement of stars, but not the madness of men.”

The chart of the South Sea Company’s stock price, and effectively of Newton’s emotional journey from greed to satisfaction and then from envy and more greed, ending in despair, is shown above.

Lesson learnt is that herd mentality kicks in after euphoric greed predominates kicking out all the sanity a person have.

Resisting such emotions is very very tough and I have to fight it out every time I am in that situation.

What worked has me may not work well for others but I had more success when the risks were higher. You can get a good price and if you can factor the risk, it comes out be a better deal.

People pay a premium when markets are good but they all give a massive discount when the markets are down.

While every one has access to the market data or media, very few are able to separate sentiments from rationality. I purchased few houses from foreclosure couple of years ago & I can’t believe that I was able to purchase houses for 10% of their value. Cash flow remains almost the same as well. So I bought few and sold them at rent-to-own with taking down payment higher than what I paid for the house. I wish if I knew more about it back then but there is always another time.

Many people won’t know that house prices in 2010 touched around 1945s level. 1945 as a reminder was post-world war II era when the entire world was going through a great depression. Economy, GDP, Population and other factors are no where closer to 1945, so that buy made perfect sense. Population, GDP was at-least double if not more in 2008 over 1945 but the house price levels were the same. Even though 2008 was a tough year but I was getting too much discount to pass.

While I don’t know if such times will ever return but if you’re patients, you can have success. As they say ” Let the price comes to you”

Summary:

Take a longer time frame while making a decision. Population is increasing so that’s a very easy factor to account for. Facts like population, inflation, GDP are easily available. We’re producing far more kids than before, incomes levels have gone up & people are working longer hour even post-retirement. Efficiency is increasing day by day in every field of life.

While US economy is growing at 2-3% per year & regardless of how slow it looks like, it is really good however it can’t be sustained for long. Though we live in the most peaceful time of history, it doesn’t take lot of time to shift things over. This is the reason, we’ve to extend our time horizon and focus on things which are sustainable in the long run.

Here is what I would be doing if I am going into the new year as an investor

Construct a thesis around a hypothesis, build a strategy on how to achieve it with a backup plan & then discipline himself in following it. Every failure or success should take you back to the working sheet to validate or invalidate his assumptions.

Thoughts of storing your cryptocurrency wallet is a scary one for the majority. There has been countless stories on how people funds were stolen with no chance to recover. Have you even looked at the process to send bitcoin from one person to another.

Number of digits that you’ve to write is insane. It’s literally impossible to type them & then only option is to copy/paste. I even still till this date, have to verify couple of times & also sweat till the funds arrive in the right place.

From trading cryptocurrencies, storing or sending funds & understanding the basic concept, we are missing out on a very wide audience due to complexities involved. Not many people go out to make their life miserable in pursuit of a better solution. As many have spoken about similarity between internet & cryptocurrency early days, I’ll recall my experiences here as well.

I got my first computer on June 9th 1998 which was a Pentium I with MMX technology. I vaguely remember the specs which were a 28.8 kbit/s, 2GB HDD, 4MB graphics card & a nice casing. I remember I had to source & wait for individual items since I was living in Peshawar.

Most interesting was the idea to get connected to internet.

Getting an internet connection was fairly straight forward but there wasn’t many free email or website providers. I remember registering a domain in 1998 through network solutions who sent me a bill later. There weren’t too many options when it come to free email & my ISP ( internet service provider) was proud of offering one for a very low monthly fee.

Here are some interesting things that I can recall

Internet was by the hour in addition to monthly subscription fee

There was different pricing for off-peak & peak hours.

I had to pay my landline company every-time I initiated a connection

You can’t use the telephone line while you were connected to internet

There was a minimum usage once I connected to the internet so even if I logged in for 2 minute, i’ll be charged for 15 min.

There was a famous handshake sound produced whenever the connection was being established. I hated it since I didn’t want any one want to know.

I wasn’t sure if I’ll be able to get through since the ISP had a fixed capacity. It wasn’t uncommon to hear & very frustrating

It took 30-60 seconds to connect. Not to mention it took couple of minutes to turn on my computer

Internet speed was around 14.4 kbit/s. In comparison today I am using 1gbps internet. 14.4 28.8 kbit/s is 0.0000144 gbps. It took over 90 minutes to download a 10MB file. Today it’s less than a second.

While Internet explorer was the default browser, I preferred netscape navigator. Netscape is considered to be “best tech product of all time”. I’ve gone from Firefox, chrome to Brave now.

There was no wi-fi so no more using the internet in the washroom.

Interestingly there are still couple of million dial-up internet users in North America today. To be honest, it wasn’t a great experience to use internet at that time, but it grew exponentially because it offered something never before. You can send emails, get updates in real time and do a video conferencing.

I got introduced to internet when it was already penetrating into house hold however still the experience wasn’t the greatest but the alternatives were even poor. In early 90’s it was super limited to a small group of geeks who had to jump hoops to get anything to work.They were versed with the concepts of TCP/IP, FTP, SMTP, POP3 , HTTP, IMAP etc, but it’s not something that was a barrier for me to enter.

Internet was written off by many pundits around that time but it has totally redefined how we live our lives. It has removed barriers in building and sharing ideas. It’s very easy to imagine now how you can order a taxi from your phone, but it looked like a fairy tales 2 decades ago. I am confident that blockchain will be able to remove barriers to build innovative financial products for the masses. Technology has direct co-relation with the improvement of human lives & once the impact reaches globally, we’ll live in a much better world.

We’re still in early days of discovering & solving problems for the financial world. Blockchain is an important component of that discovery. It’s an evolution & I am excited to experience it. We’re getting better day by day !

How many of you experienced the dial-up internet. What’s your favourite memory ?

Bitcoins was a hope of beacon in the world of crazy inflation that’s impacting every one. Since bitcoin isn’t tied to any country monetary policy it’s only worth what believe it to be worth it. Though it has consistency outperformed every legacy asset on a longer time horizon, it’s still far from mass adoption and one the major reason is price fluctuation.

Here are some of the bitcoin price crashes

2017 was the craziest year for cryptocurrencies where we saw crazy gains of 10,000X but 2018 wiped off everything. This led to party moment for few but a nightmare for many. Fingers on the argument that bitcoin as a storage of value were raised & classic example of tulip mania was back in the market. It’s hard to argue with the pessimists because bitcoins doesn’t have any underlying fundamentals behind it. More & more negative media however has attached a taboo towards this revolutionary technology through which money can be programmed.While I personally have seen crashes multiple times over last 7 years, it’s tough to see market take a toll like this. Overall I am bullish on the cryptocurrencies however sanity has to prevail. It’s hard to deny the advantages cryptocurrencies provide but price volatility is keeping them off field for many serious players. While it’s exciting to see the upside swings, not everyone has an investor mindset. Since majority of the countries regulations are hostile towards cryptocurrencies, volatility keeps the institutional investors further away. There has been one thing certain about bitcoins & that’s volatility. There are many funny memes & jokes around but the following one is my favourite

A boy asked his bitcoin-investing dad for 1 bitcoin for his birthday.

Dad: What? $15,554??? $14,354 is a lot of money! What do you need $16,782 for anyway?

There is an interesting case of token velocity which is super high when someone is using it as the currency and doesn’t want to hold. In case of cryptocurrencies, if you’re holding for long you’ll get a HODLER ( Hold On for Dear Life). HODLERS are generally regarded as highly respectable in the industry because they’re considered to be in for the long vision rather than flipping. Everyone loves to HODL, however the scary swings aren’t for the faint hearts.

Welcome Stable Coin which does take care of the volatility problem by being pegged to a fixed value such as fiat or commodity. This is the answer to every day users who don’t want to be exposed to price movements. It does fulfil the basic functionalities of money which are

Means of exchange

Unit of Account

Storage of value

Transaction in cryptocurrencies have been complicated due to fluctuations & stable coins are supposed to put a stop to that. It’s almost impossible to transact in exact amount. Stable coin prime job is to protect the immutability of the transaction value. This also makes a strong case for cryptocurrencies and graduates it into a mature storage of value. 2018 has been a good year for stable coins which mushroom growth of stable coin provider. Everyone have their own way of approaching the solution but majorly they can be divided into two which are further subdivided into two. The two solutions are first divided by the way they’re designed and then by the virtue of their functionality. Overall they serve the same purpose, provide stability in the price of the user-desired assets.

There are two major types of stable coins philosophies

#1 – Centralized

#2 – Decentralized

Centralized coins are the one where there is a centralized entity keeping possession of the assets while in decentralized case, it’s generally a smart contract stabilizing the value.

Centralized

Centralized coins are issued through a financial institute who has the custody of the asset backing them. There are two major types of assets which are considered colletral while issuing stable coin

Fiat

Commodities

Fiat backed

This is the most common type of coin where the stable coin is issued against fiat currency by a centralized financial institute. Here are the features of fiat-backed stable

It’s value is pegged to a fiat currency such as USD in a fixed ratio such as 1 stablecoin would be equal to 1 USD. USD is the most common pair but other pairs are also available.

Financial institutes at any time is in the possession of the fiat currency backing the coin.

Transaction may run off-chain or it’s own private or dedicated public chain

Total collateral should be equivalent to circulating supply at any given time.

Technical wise, this is the most simplest way to issue a stable coins since the financial institutes just issues coins based on the amount they’ve. They are tradeable on exchanges and redeemable by issuing financial institutes. Trust in the entity backing is super important. Financial institutes does have an incentive in increasing the fiat backing because they can earn interest on the money without any risk. Even at 2% interest for 1 billion deposit, they’re earning 20M/year risk free. Cash handling cost is much lower than this making it a cash cow the financial institute. Cost involved are generally occured by the financial institutes anyways. We’ll see more and more financial institutes issuing similar kind of stable coins.Due to centralized nature, if the financial institute backing the coin has any problem, it’ll have directly impact on the the stable coin issued by them.

Commodities backed

Similar to fiat, there are stable coins which value is pegged to commodities they’re backed by. Most popular form of commodity is gold followed by silver, but we’ll be able to see other precious metals & petroleum based coins as well.

It’s value is pegged to an asset such as gold in a fixed ratio such as 1 stablecoin is equal to .01 ounce of gold. Gold is the most popular but silver and other exotic commodities are also being issued.

Financial institutes at any time is in the possession of the commodities backing the coin.

Transaction may run off-chain or it’s own private or dedicated public chain

Total collateral should be equivalent to circulating supply at any given time.

Technical wise, it isn’t difficult either but the fluctuating price of underlying asset does require financial management and generally the storage cost is higher as compared to fiat. Commodities which are generally supported by stablecoins has to be fluid and tradeable on exchanges. They are tradeable on exchanges and redeemable by issuing financial institutes. Trust in the entity backing is super important. Having higher deposit strengthen the balance sheet which empowers the financial institute be leverage. Similar to fiat-backed stable coins, we’ll see more of commodity based coins as well.

Decentralized Stablecoins

Decentralized coins are not controlled by a single entity but more by code that stabilizes the value. There are multiple 3rd parties who have to participate in order for the value to be stable.

Cryptocurrency backed

Most common form of decentralized stable coin are backed by cryptocurrency. There isn’t major difference between cryptocurrency and fiat backed stable coins in terms of logic but due to nature of the transaction everything is done through smart contract & is on-chain. User put up their funds as collateral which is generally significantly higher than the stablecoin issued to cover up in case there is a flash crash. Despite higher loan to value, there are still liquidation events which even has more impact on the price and has lead to black swan events.

Here are some of characteristics of stablecoins

Value is pegged to fiat but it’s pegged by a cryptocurrency

No centralized body is in control of collateral but it’s locked through smart contract & is executed on-chain

There are additional supplementary instruments and concept of oracle which keeps the price stable. These oracles have act more like a bounty hunter which is looking for liquidations and make a small profits whenever it is able to execute properly

Though it’s very similar to any centralized stablecoins in terms of mechanics, risks are far higher. Biggest risk is code exploitation which can lead to collapse of entire system. Though there are constant audits, but still history is full of breaches and hacks. Here the stakes are much much higher. Smart contract doesn’t execute by itself but requires a third party execution so the system has to rely on them. If they fail to act in time, liquidations might not happen in time destroying the peg value. Easiest option is to have a very high value of collateral with respect to loan however it may make tit unattractive since investors are looking to leverage up not the other way around.

Seigniorage (algorithmic)

They’re similar to a Decentralized Autonomous Organization ( DAO) which controls issuance and pricing, which are referred to as seigniorage-style (or algorithmic) stablecoins. They’re completely digitalized and non-dependent on any collateral whatsoever. Supply, demand & target price is controlled by the code which makes it truly decentralized and no regulatory oversight. Both of these features increases its ability to scale as compared to counter part solutions since there are not any additional collateral requirement with supply increase

Here are the major features

Full decentralized,

High scalable,

Executed on-chain,

Cheaper to maintain the price immutability due to lack of collateral requirement

It operates on the basic principle of supply and demand where coins are issued if there is enough demand & destroyed if the demand drops. This issuance and destruction keeps the price stable. Generally if the price goes down. Bonds are issued and if the price goes up seigniorage shares are issued. This is most exciting form of stablecoins but haven’t been in production yet.

There are also creative proposals on how to achieve stability while keeping the decentralization property and it’s a work in progress.

Concerns:

Stable coins aren’t stable

There hasn’t been a single example of stable coin that have been successful at keeping the exact peg for extended period of time. Multiple times they’re traded few percent above or below their actual value. Theoretically they’re great but they’re prone to market fluctuations as well. In one case, value of a stable coin has dropped by 70%.

Do they bring stability ?

Bitcoin does have a connection with alternative coins when it comes to price movement so generally the overall market doesn’t move much with respect to each other. Bear and bull markets are correlated. Stable coins adds a different dimension to market pricing where people can bring in fiat and take a short/long position making the market extremely unstable. So with stable coins, the term shouldn’t confused with the fact that it’ll bring stability to the market. It just keeps the value stable for the holder of that specific coin

3. Vulnerable

It is a new concept and haven’t been tested over long period. There are chances that one of them will break causing a spiral downward market crash. It has happened in the past but they were not as popular at that time having minimal impact. Even decentralized coins are prone to hacks Stable coins generally require us to trust a central third party. In case of centralized coins, there are always risk of custodial going illiquid.

Pursuit to perfection

Cryptocurrencies basic moto is decentralization but there isn’t a fool proof system to get a perfect solution. We’re far from perfection but we have came a long way. Stable coins are on the rise with over 2 dozens companies working on the solutions. Every has a unique approach and hopefully we’ll have a perfect solution soon. Stable coins are the holy grail of crypto and is a necessity piece in the puzzle. With extreme volatility in cryptocurrencies, it would encourage people to get in and out of the market whenever they want. None of the solutions are reliable so they’ should be only treated as an ad hoc solution. Right now it’s limited to startups, but bigger financial institutes will move into the game and I won’t be surprised if countries start issuing their own digital currencies on the principle of cryptography. Rome wasn’t built in a day & future won’t be either. It’s an evolution towards better & better

HODL is a term that got popular through a forum post where a person claimed to hold the bitcoins forever once the markets crashed. HODL stands for Hold On for dear Life on in simple word never selling them. Now either it was intentional or unintentional, HODL did become famous in the cryptocurrency industry.

King Leonidas from 300

Out of the total 17M bitcoins in existence, 9M haven’t moved in the last 12 months. This represents around 53% of the total bitcoins but I am confident that this number is close to 75% in actual. It’s not possible to get the data on individual users who store their bitcoins on the exchanges

Source : Bitinfo Charts

While HODLing does promote the message of hope & avoid capitulation in bear markets, it isn’t right for the network bitcoin. Bitcoin network runs due to support from miners who mines bitcoins in hope of getting bitcoins in return.

If the blocks are solved exactly 10 minutes apart, all the bitcoins will be mined by 2140 which is 122 years from now. Margin of difference actually would be +/- 10 years.

I suspect if we go that far but for a moment let’s consider we did. In that case, there are no more bitcoins to be mined so miners make money by validating transactions. Now imagine every one is HODLing and there are no transactions happening at all. There isn’t any incentive for miners to exist because the economic incentive has collapsed.

Bitcoin network strength depends on the hashpower supporting network and with the departure of miner, there isn’t any network or just a weak network. HODLing is celebrated & cheered upon in the industry, however it’s a threat to the fundamentals of cryptocurrency.

If you consider bitcoin a instrument for Storage of Value then HODLers are the #1 or Most Valuable Users ( MVP) for bitcoins.

While HODL certainly make sense to avoid the panic attacks in tough markets, it doesn’t make sense over life time of any other asset that doesn’t generate dividend. Real estate being the #1 fav HOLDing asset.

So while times are time, don’t panic & when times are great, it’s always good to take off some profits off the table. Capitulate & HODL both are bad from economical point of view

What’s your strategy when the times are great or when they aren’t that great !

2018 has been the worse year for blockchains if you look at the price. Unfortunately, measurement of success in this industry has been measured by market cap. It has roughly lost 85% of its financial value within12 months which may be among the worst performance for any asset in the modern history. There are many other indicators showing all time worse situation for the industry. Question is it all over for blockchain or we can recover from here.

Capital preservation is the #1 reason behind success of wealthy people. If you look at the chart below, it shows how much gains are required to make up for the loss. Summary is It’s much difficult to make up for a loss.

Gains required to makeup for the loss occured

If you look at the history of bitcoins, it has been pronounced dead 100s of times. I’ll do a blog post on death announcements vs price action some later day. Bitcoin has lost 85% or more around 5 times now in last 6 years. Defying every traditional law of finance, it has however recovered strong every time. This exponential rise isn’t alien in the tech world and hockey stick pattern is fairly common.

I got into bitcoin purely because of FOMO 7 years ago. I couldn’t resist staying out while watching everyone around me flaunting about their crazy gains. For me it was unreal & there was no chance I was going to lose. Sadly, I bought my first bitcoins at All Time High (ATH). Bitcoin crashed the very next day losing 50% of the value. I’ll be honest I was really upset over what just happened and pessimism was at all-time high. Fear of losing everything almost made me sell it, but then I figured I’ve already lost 50%, what if I lose the another 50%. Bitcoin at that time was already up by some crazy 12X or so, so there was a hope it can do it again. That was almost 7years ago when bitcoin dropped from $260’s to $40’s.

Looking back, it seems very easy to make the decision toHODL, but it’s not an easy choice when you’re in that moment. It’s very simple to classify the early bitcoiners as lucky but as a matter of fact, they’ve scars all over them. Perseverance in the end paid off for majority of them, but it was super difficult back then.

Bitcoin is lucky enough to have a cult following composed of libertarians, economic freaks & tech geeks who’re in for ideology rather than monetary benefits. This bear market has little impact on them. While everyone is hurt, they’ll continue to BUIDL. With every price rise, there has been a new set of people who come in but as things start to fall apart, they’re the first to pack their bags. In case of a disaster, it’s the tourist who leave first. Habitants stay and focus on rehabilitation.

Photocredits ” by James Nachtwey

Cryptocurrency is going through its tough time when it comes to valuations however adoption is all time high. There hasn’t been a time in history when there were this number of intelligent brains working on brilliant ideas. I’ll call it crypto winters where majority of the project don’t have enough resources to survive. It would be a litmus test that’ll differentiate the boys from men. Let’s see how long this survive & most importantly who survives.

Terms Used:

HODL – Hold on for Dear Life. A term very popular referring to holding on the

bitcoin regardless of whatever is the price.

BUIDL – Derived from HODL meaning Build for Dear Life. Meaning keep on building

regardless of whatever is the price

FOMO – Fear of Missing Out which makes you take an irrational risk without any due

diligence in fear of missing on a massive potential upside

ATH –

All time high means you’re the sucker who bought at a price at which you may

not be able to offload.