5 years ago, we installed the first bitcoin ATM in Toronto at Decentral. These 5 years passed by quickly. I am humbled by the people I met, experiences I had & opportunities I got through that experiment.

That venture started as a fun weekend project that turned into a business. Today it’s a thriving company. I’ll cover that story later but today I’ll write about why I think Bitcoin ATM is a killer use case for cryptocurrencies.

It’s fairly easy to buy bitcoins in today’s age & date however it wasn’t the situation in 2013. We had disasters like MTGox in addition to some shaddy exchanges which wanted you to transfer funds to an offshore entity. At time it used to take months before you can see your money in bank account. Bank accounts were also getting shut down for just dealing with an exchange.

Idea behind Bitcoin ATM was very simple. It’s a simple machine that converts fiat into bitcoins & vice versa. It was considered one of the most unpopular startups due to it’s nature. Like here everyone is building next generational cryptographic solutions & here we were cranking steel boxes with cash recyclers. In the utopia world of crypto, it was hard to make an impression & was laughed upon.

5 years passed by & today there are over 4,000 BTMs serving performing millions of transactions every year. For majority of people, their first interaction with bitcoin was through Bitcoin ATM. I do often come across stories of how people use these machines. It’s one of the most important component of the entire cryptographic currency movement.

I still to date believe that one of the most weakest link in the decentralized financial world is traditional banking. Today if banks shut down any exchange bank account, they’re done. Building an exchange using a bank is like building an AirBnB in the lobby of Marriot

Here are some interesting use cases around how these Bitcon ATMs can do more than just

Bank Account

People can buy stable coins through it & store it in their wallet. Banks are generally only interested in banking the top 1% so there is a big number that can be served.

Infrastructure as a Service

These BTMs can be used to offer services to unbanked directly from these machines. Companies can built applications targeting this market segment & BTM can serve as an intermediary

Money Transfer

Despite digitisation majority of the money remittance is done in cash. 80% of the expenses for a money transmission company are due to location & KYC. BTM can slash these expenses by 95%

If you look at any financial institute, they’ve to dependent on SWIFT or central bank network for transfer of fund. Through BTMs foundation of an independent financial system that be laid which can be built parallel to legacy. This system have it’s own rail tracks allowing more flexibility. There is a bigger opportunity to build a network of BTMs which can perform any function that any other financial institute can perform.

These BTMs can have cash recycler and in an ideal scenario there isn’t any need to replenish or fill up the cash. They can independently operate & replace any branch effectively improving profitability 5X.

Have you ever used a Bitcoin ATM or is there a Bitcoin ATM nearby yours ? Also what else do you think these BTMs can do ?

Financial cycles are often misunderstood by majority. It’s a zero sum game where transfer of money takes place from one entity to another. It’s combination of analysis, research but luck outplays every other factor. Markets react irrationally majority of the times.

Either you’re a fund manager or an individual managing your personal portfolio, what’t the #1 question that goes through your mind.

“Is this a great time to exit or enter”

There are three types of sentiments that exist in the market at any given point of time.

Market Neutral

Bullish

Bearish

Every one in the market has a conviction behind his decision once he is able to identify the trends based on the information he has. General trend is to follow the trend and don’t ride against the wave, however if you look at history biggest gains are made when people went against what market was doing.

Quote from 2004 Annual Shareholder Letter for Berkshire Ha

Warren in the letter explained how well the stock markets have performed & index funds was the best investment that people could’ve made, but he outlined the 3 biggest traps for any investor

Trading too much & incurring fees

No or little stock analysis

Poor skills at timing the market

He also mentions that though these are the obvious ingredients for failure, they’re added to the receipt of success repeatedly

Gold mines are found when you’re patient and have your own strategy. I’ll cover the following

Why is it a good idea to go against the market

Why crashes always follow bubbles

Why risk-free is actually the most riskiest approach

Before I dive into more details, let’s start with the basic notion behind investor mentality. He is always looking for one thing

Buy assets with high value at a low value. Delta between actual value & value he paid is the profit

My job is to invest in a wide variety of assets & construct a portfolio with different strategies to yield results beating the market average. History suggest than less than 33% of the people are able to beat the market average, but the returns for 33% are so high which keeps the remaining 67% in the game. Luckily, I am among the 33% so far, but I could be on other side of the table anytime.

Luck plays an important role in any investment outcome regardless of how much research one has done. Some are better at guessing by chance or by research, but no one has a crystal ball to predict accurately. Best thing an investor can do is to construct a thesis around a hypothesis, build a strategy around it with a backup plan & then discipline himself in following it. Every failure or success should take him back to the working sheet to validate or invalidate his assumptions.

While research is good, the biggest factors involving the market cycles are large-scale economical, geopolitical or market-related events including but not limited to security, war, military take-overs, political instability, natural resources discovery, big trade agreements or a technological breakthroughs. With advent of internet, every one has access to this information & now it’s up-to their intellectual ability to absorb, assess and guesstimate the impact on the markets.

There are multiple types of traders. It could either be day-trader, long term investors or just wicks scalper. Regardless of whoever you are, it’s the exact same mission. Beat the market with your decision. You can either be investing in hope of price increase, generating cash flow or just diversifying your asset to preserve capital, but every move you determine is nothing but just a speculation. Everyone is hoping to be smarter than others, but that rarely happens.

In the past, I acquired assets which were a steal but also picked up garbage that still to date I can’t believe. Biggest jackpot is when you’re able to time well. It’s like striking the ball in the right direction from middle of the bat. It’s super hard to time it well, so best is to have an exit and entry price & not worry about over optimising your gain. Just minimize your losses.

So what’s a cycle? They’re similar to any wave that you see at the ocean which comes and go however waves can be bigger or smaller. Despite their unpredictability, if you look at a longer time frame, you can have some level of confidence of the future. Example is night comes after day, but the time sun rises and set changes from season to season. We may or may not have a White Christmas in Toronto, but ruling out snow in January/February is very hard.

It’s easier to be right in the longer time frame while very difficult to be right in a short time frame. Reward to be right in a shorter time frame is higher but Risk reward ratio just doesn’t justify the action.

Today we’re fortunate enough to have access to so much information that we can plan our day very concretely. Though we don’t know if it’ll snow on 25th December, but history shows that there isn’t any January without any snowfall.

While it becomes super hard to predict a specific trend during the day, long term cycles are fairly easy to identify. We were in the longest bull run in the history with every assets giving returns that were unprecedented in the history for the last 10 years. General public does exactly opposite to Buffet suggested. People will jump into an asset class when it has already reached the peak and will shy away from getting into an asset when it has bottomed out.

Bubble-Burst cycle keep on repeating rewarding the smart, lucky and patient people while taking it away from the people on the other side.

Focus on Long term:

“There are only patterns, patterns on top of patterns, patterns that affect other patterns. Patterns hidden by patterns. Patterns within patterns. If you watch close, history does nothing but repeat itself. What we call chaos is just patterns we haven’t recognized. What we call random is just patterns we can’t decipher. what we can’t understand we call nonsense. What we can’t read we call gibberish. There is no free will. There are no variables.” ― Chuck Palahniuk

If we look at the great depression, dot-com bubble, 2008 recession or any other similar event, there are many commonalities. Biggest one is the rate at which things are changing. Similar to body, economies or growth can’t rely on steroids for long. You can have a shot here and there but overall it should have merits. Back in 2013, I recall there were only 2-3 investment firms which remained in single digits till 2017 where every one wore the hat of Blockchain VC with reported number of more than 100 in 2017.

Mushroom group of these wanna be investors was toxic because companies were raising millions in seconds where they won’t have even be able to raise 10k from traditional industry. Result bubble burst and cryptocurrencies have lost 90% of it’s market cap. This isn’t the first time it has happened and probably won’t be the last one. These however does act as a filter for part-timers. I read on this topic here

While things generally do recover, it may take much longer in few cases. Though there is more VC invested today in startups than 2008 but the house ownership hasn’t returned to even closer to numbers of 2008.

Overall, with population growth economy has to grow and research shows the poverty levels are improving as well, so there isn’t a mystery behind achieving reasonable growth. Perseverance is the goal. As they say whatever that goes up must come down.

Biggest challange with the short term mentality is to understand investor psycology. Research shows that 90% of the decisions that we do are irrational. Very few people are disciplined and our spontaneous decisions make or break our lives. We have our own mood swings, good and bad days & in few extreme cases it’s more like a pendulum from unbounded euphoria & bottomless despair.

#1 reason for short term market mentality is those pendulum mood swings. It could be euphoria-driven greed that lead you to go all in or despair-driven fear that lead you to sell everything. Either people think this is once-in-a-lifetime opportunity or the world is going to end. Biggest mistake people make is when they convince themselves that this time will be different.

Even though your heart is saying that markets are irrational, you get in for a swing trade. It just take one person to panic and the stack of cards start to follow down creating a dominos effect. Fear of greed or fear or losing, both are dangerous.

Though it’s super easy to comment on it, when you’re in the moment, it’s very hard to resist even for the best of the best.

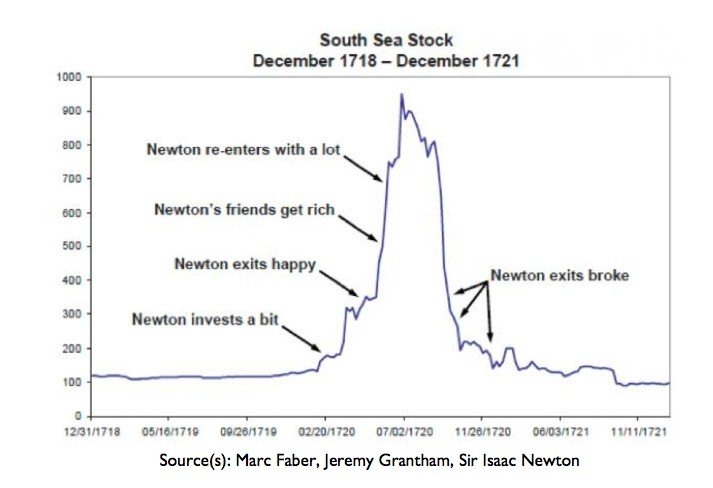

An early example is the case of Sir Isaac Newton and the South Sea Company, which was established in the early 18th Century and granted a monopoly on trade in the South Seas in exchange for assuming England’s war debt.

Investors warmed to the appeal of this monopoly and the company’s shares began their rise.

Britain’s most celebrated scientist was not immune to the monetary charms of the South Sea Company, and in early 1720 he profited handsomely from his stake. Having cashed in his chips, he then watched with some perturbation as stock in the company continued to rise.

In the words of Lord Overstone, no warning on earth can save people determined to grow suddenly rich.

Newton went on to repurchase a good deal more South Sea Company shares at more than three times the price of his original stake, and then proceeded to lose £20,000 (which, in 1720, amounted to almost all his life savings).

This prompted him to add, allegedly, that “I can calculate the movement of stars, but not the madness of men.”

The chart of the South Sea Company’s stock price, and effectively of Newton’s emotional journey from greed to satisfaction and then from envy and more greed, ending in despair, is shown above.

Lesson learnt is that herd mentality kicks in after euphoric greed predominates kicking out all the sanity a person have.

Resisting such emotions is very very tough and I have to fight it out every time I am in that situation.

What worked has me may not work well for others but I had more success when the risks were higher. You can get a good price and if you can factor the risk, it comes out be a better deal.

People pay a premium when markets are good but they all give a massive discount when the markets are down.

While every one has access to the market data or media, very few are able to separate sentiments from rationality. I purchased few houses from foreclosure couple of years ago & I can’t believe that I was able to purchase houses for 10% of their value. Cash flow remains almost the same as well. So I bought few and sold them at rent-to-own with taking down payment higher than what I paid for the house. I wish if I knew more about it back then but there is always another time.

Many people won’t know that house prices in 2010 touched around 1945s level. 1945 as a reminder was post-world war II era when the entire world was going through a great depression. Economy, GDP, Population and other factors are no where closer to 1945, so that buy made perfect sense. Population, GDP was at-least double if not more in 2008 over 1945 but the house price levels were the same. Even though 2008 was a tough year but I was getting too much discount to pass.

While I don’t know if such times will ever return but if you’re patients, you can have success. As they say ” Let the price comes to you”

Summary:

Take a longer time frame while making a decision. Population is increasing so that’s a very easy factor to account for. Facts like population, inflation, GDP are easily available. We’re producing far more kids than before, incomes levels have gone up & people are working longer hour even post-retirement. Efficiency is increasing day by day in every field of life.

While US economy is growing at 2-3% per year & regardless of how slow it looks like, it is really good however it can’t be sustained for long. Though we live in the most peaceful time of history, it doesn’t take lot of time to shift things over. This is the reason, we’ve to extend our time horizon and focus on things which are sustainable in the long run.

Here is what I would be doing if I am going into the new year as an investor

Construct a thesis around a hypothesis, build a strategy on how to achieve it with a backup plan & then discipline himself in following it. Every failure or success should take you back to the working sheet to validate or invalidate his assumptions.

Thoughts of storing your cryptocurrency wallet is a scary one for the majority. There has been countless stories on how people funds were stolen with no chance to recover. Have you even looked at the process to send bitcoin from one person to another.

Number of digits that you’ve to write is insane. It’s literally impossible to type them & then only option is to copy/paste. I even still till this date, have to verify couple of times & also sweat till the funds arrive in the right place.

From trading cryptocurrencies, storing or sending funds & understanding the basic concept, we are missing out on a very wide audience due to complexities involved. Not many people go out to make their life miserable in pursuit of a better solution. As many have spoken about similarity between internet & cryptocurrency early days, I’ll recall my experiences here as well.

I got my first computer on June 9th 1998 which was a Pentium I with MMX technology. I vaguely remember the specs which were a 28.8 kbit/s, 2GB HDD, 4MB graphics card & a nice casing. I remember I had to source & wait for individual items since I was living in Peshawar.

Most interesting was the idea to get connected to internet.

Getting an internet connection was fairly straight forward but there wasn’t many free email or website providers. I remember registering a domain in 1998 through network solutions who sent me a bill later. There weren’t too many options when it come to free email & my ISP ( internet service provider) was proud of offering one for a very low monthly fee.

Here are some interesting things that I can recall

Internet was by the hour in addition to monthly subscription fee

There was different pricing for off-peak & peak hours.

I had to pay my landline company every-time I initiated a connection

You can’t use the telephone line while you were connected to internet

There was a minimum usage once I connected to the internet so even if I logged in for 2 minute, i’ll be charged for 15 min.

There was a famous handshake sound produced whenever the connection was being established. I hated it since I didn’t want any one want to know.

I wasn’t sure if I’ll be able to get through since the ISP had a fixed capacity. It wasn’t uncommon to hear & very frustrating

It took 30-60 seconds to connect. Not to mention it took couple of minutes to turn on my computer

Internet speed was around 14.4 kbit/s. In comparison today I am using 1gbps internet. 14.4 28.8 kbit/s is 0.0000144 gbps. It took over 90 minutes to download a 10MB file. Today it’s less than a second.

While Internet explorer was the default browser, I preferred netscape navigator. Netscape is considered to be “best tech product of all time”. I’ve gone from Firefox, chrome to Brave now.

There was no wi-fi so no more using the internet in the washroom.

Interestingly there are still couple of million dial-up internet users in North America today. To be honest, it wasn’t a great experience to use internet at that time, but it grew exponentially because it offered something never before. You can send emails, get updates in real time and do a video conferencing.

I got introduced to internet when it was already penetrating into house hold however still the experience wasn’t the greatest but the alternatives were even poor. In early 90’s it was super limited to a small group of geeks who had to jump hoops to get anything to work.They were versed with the concepts of TCP/IP, FTP, SMTP, POP3 , HTTP, IMAP etc, but it’s not something that was a barrier for me to enter.

Internet was written off by many pundits around that time but it has totally redefined how we live our lives. It has removed barriers in building and sharing ideas. It’s very easy to imagine now how you can order a taxi from your phone, but it looked like a fairy tales 2 decades ago. I am confident that blockchain will be able to remove barriers to build innovative financial products for the masses. Technology has direct co-relation with the improvement of human lives & once the impact reaches globally, we’ll live in a much better world.

We’re still in early days of discovering & solving problems for the financial world. Blockchain is an important component of that discovery. It’s an evolution & I am excited to experience it. We’re getting better day by day !

How many of you experienced the dial-up internet. What’s your favourite memory ?

So uber launched self driving cars yesterday. It is pretty interesting move since it will basically kills the jobs that they created in the first place. So with Uber every individual can drive for them as per their own schedule, but with self driving cars, there is no schedule. (more…)

Microsoft just announced to acquire LinkedIn for $26 Billion which is almost 50% higher than the public market valuation. For the sake of comparison, Google purchased YouTube for $1.65 billion 10 years ago. Facebook paid $715 million for Instagram in 2012 and $19 billion for WhatsApp two years ago. (more…)

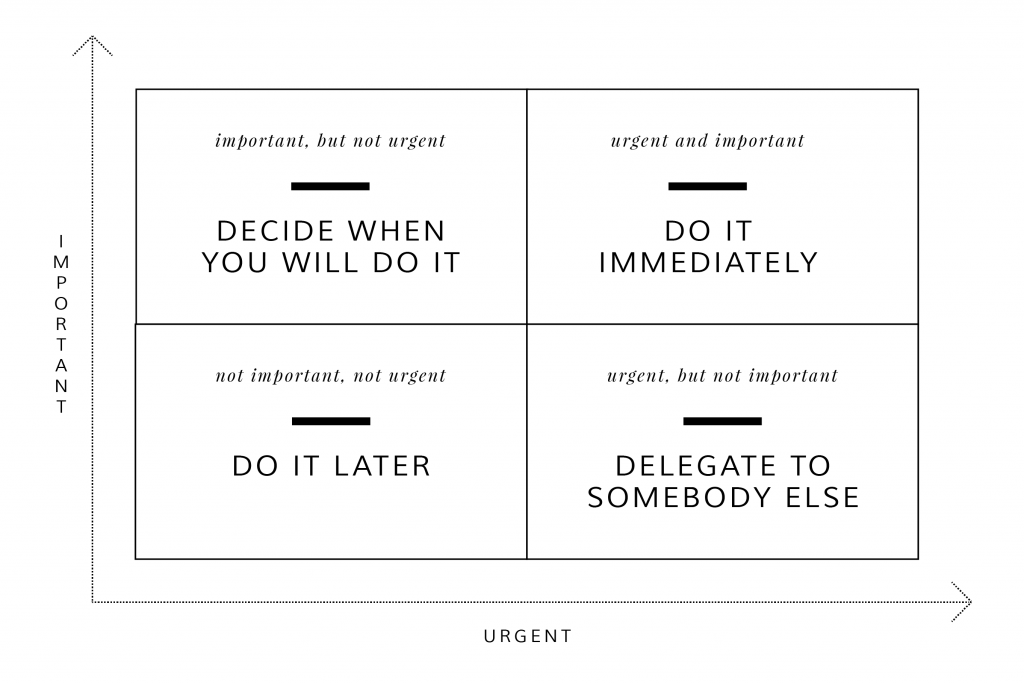

Time is the most limited commodity that any successful person have & time management is one of the most sought after skill for majority of us. Urgent & Important are the two major parameters used in prioritizing where to focus our resources on.

Eisenhower matrix is ever-green cheat sheet for any one looking to help prioritize their day. Biggest issue we struggle with is “urgent” taking priority over “important”.

If you give some one two tasks with following – Task A is urgent – Task B is important

99% of the times, they will go with the urgent one. There could be multiple reasons for this behaviors, but following two are the most common one.

– Urgency creates emergency giving you the adrenaline rush for the day – It is easy to get motivated while accomplishing a task that is time driven because it could be quantified

The most urgent decisions are rarely the most important ones. – Dwight D Eisenhower

However, while focusing on urgent task, we oversee important tasks requiring our attention. It could be a business goal as well as personal goal. Such as joining a gym, going on a vacation, spending time with your family, calling an old friend or be by yourself. Even in business, we mightn’t have updated our website or done a SWOT analysis or the most important one – sitting down with the team over dinner.

So next time, there is a choice between Urgency or importance, chose wisely!

They also changed their stance on frequency of changing the interest rate. Earlier they indicated that they would change interest rate 4 times in 2016, but it was not well received in the market. Now they have backed-off to resonate with their counterparts. While it’s not as exciting, this will bring stability to the economy. Stable interest rates are boring but it is good in the long run. Feds assurity about the stable interest rate will bring confidence to investors so they can plan and forecast better. Low interest rate acts like a catalyst to economy by encouraging people to rotate the money and invest rather than just leaving it in fixed deposit.

The new stanceis similar to what European Central Bank ( ECB) and Bank of Japan are taking to boost their economy. This however would affect the USD strength against other currencies. People will prefer to invest in alternative assets, making USD less in demand as an asset class. There are both pros and cons of weaker currency, but overall there are always advantages for a stable currency. So if you are an importer, you should be unhappy and if you are an exporter you should be happy. Historically, Fed movements can be well predicted in advance, which is a good indication of them being more realistic with the economic condition. In near future, we should be assure that interest rates are going to be stable and FOMC meetings would have no exciting news to share.

The financial services industry is a cutthroat market with razor-thin margins, making it one of the toughest industries in which to generate profit. Yet, for Fintech startups, it is one of the least chartered, most lucrative sectors.

Accenture recently reported that fintech investments grew 201 percent in 2014 compared to the previous year. As a comparison, overall venture capital investments grew only 63 percent in the same period.

There is little doubt that today’s financial systems are inherently complex, outdated and inefficient. The potential to innovate within this sector has never been higher. Because of wide-scale technology adoption, mobility and digital money, banking and financial institutions are facing imminent threat from fintech startups for products such as loans, money transfers and stock trading.

Indeed, customers today have more options with third-party financial service providers when it comes to choosing products. However, running a profitable fintech startup is very challenging.

With higher cost of customer acquisition, most fintech startups are surviving on venture capital funding. Because they are new, Lifetime Value (LTV) is not yet realized. It would be very difficult for a financial institution to survive on a single product, so they must diversify their portfolio of services to maximize LTV.

No one can unequivocally predict the future. However, here three ways to stay current in the financial services industry.

Existing Banks Must Innovate

Banks are not as slow as they are perceived to be. In fact, they are very smart at focusing on revenue-generating sectors and ignoring less-profitable ones, such as money transfers, small loans, etc. While startups in the space are claiming to take over the money-transfer business from banks, this area is purposely ignored by the banks.

As an example, Western Union, a money-transfer company that controls approximately 18 percent of the money-transfer market, had revenues of $5.6 billion last year, while JP Morgan earned $102.1 billion.

Lending, on the other hand, is considered a profitable service, but bank shares within this sector are decreasing. As per a Goldman Sachs estimate, 20 percent of money lending will move to alternative finance companies, costing the banks $12 billion in lost revenue (this is 7 percent of the total profits for the banking sector).

Banking and financial institutions are facing imminent threat from fintech startups.

Banks have the resources to acquire the best talent, infrastructure and whatever it takes to get the job done. However, the scale of business reduces chances of upward mobility. Fortunately the banking sector has an extremely low churn rate when it comes to core products — deposits and lending.

As per a Consumer Intelligence survey report, approximately 3 percent of people change their banks in any given year. Other findings indicate that 57 percent of people have been with their banks for the last 10 years, and 37 percent are trusting their banks even after 20 years.

Banks have the leverage of a huge customer base, experience, licenses and deep pockets. They will try to stay relevant, but if they fail to innovate faster, they could be looking to acquire winners in the niche product markets. In this case, financial companies retain the monopoly.

The Emergence Of Fintech Banks

The biggest challenge for any company is to acquire customers. High acquisition cost can kill any venture. However, once you have acquired a satisfied customer, you can always cross-sell other financial products to maximize ROI. For instance, a lending platform can sell mortgages. Once they are selling mortgages, they can sell insurance and ancillary services, and so on.

Banks initially started with deposits and lending, diversifying their product offerings later on. Most startups are currently focused on a singular niche product to take incumbent market share away from a profitable line of business. Because of the technology-centric nature, they are better at analyzing data and offering better products and a better customer experience.

The key here is to expand horizontally by being equally good at it.

If you are already using a money-transfer company, why not store money with them, as well? Or, if you are a lending platform, why not take customer deposits to strengthen the deposit base? Rather than going through resource-intensive banking licenses, there are many financial institutions open to giving access to their licenses. This will not just be limited to fintech startups, but also social giants like Facebook, WeChat, etc. that are eager to enter the financial space.

In this case, a technology startup can be the bank of future.

3.0 Brokerage Banks

There is no secret sauce to running a financial institution, but the bottom line is always the same: Keep your operations as efficient as possible.

However, it is almost impossible to be good at every product facet. A lending platform might not be able to beat their competition in the money-transfer space, and vice versa. Similarly, the lending company may struggle when it has to issue insurance.

If banks are unable to innovate faster or startups are struggling with distribution, this creates an opportunity for a marketing company to consolidate all the services under their brand name.

There is little doubt that today’s financial systems are inherently complex, outdated and inefficient.

Rather than developing any expertise, they just take the role of an intermediary and route the transactions through the best possible partner. For example, they may direct a money transfer of $150 to Pakistan via one of their partners, whilst they might use another provider for mortgages. It is not an uncommon practice in other industries. However, such an amalgamated model is rarely found in the financial space if you are just a marketing company.

It would not be out of place to say that by 2020 you might be a marketing brand, showcasing and selling repurposed/repackaged products to the consumers — but at the back end, you are neither a technology company nor a bank.

There might not be enough space for multiple players to exist without venture capital in this cutthroat industry. It will be interesting to watch who wants to be the bank of 2020.

But be it a financial, technology or marketing company, the customer will always win.

Banks are boring & claim to be next generation bank is rarely heard in startup world. Banks were born out of need to store the cash safely. Banks generally have a very good perception of trust & security among masses which led to position themselves as one-stop shop for anything financial related. Over time they built the brand , distribution & resources to up-sell other financial products such as loans, insurance, money transfers etc.

As any other business, competition have started to hurt the banks. However, new entrants are not keen to attack the core competency of the bank i.e holding people’s money. The main reason behind lack of competition is the resource intensive regulatory process. With low ROI. it’s not worth the effort for startups. Although bank fees brings lot of revenue to the bank, holding money is not profitable. It’s more of a liability than an assets.

Startups will take away the profit-making products of banks leaving them with liabilities to hold cash only

When it comes to retention, banks are doing really good job. When was the last time you changed the bank ? As per a survey, approximately in any given year 3% of people change bank. While 57% of the people are with their bank for last 10 years, 37% people are still trusting their bank even after 20 years.

For startups, it is easy to launch other financial products due to less barrier to entry in terms of regulations. In no specific order, popular products are

Lending

Remittance

Bill payments

Credit card processing

Insurance

Hedge funds

Credit cards

Lending being the most popular product, FinTech startups are focused on creating the most efficient P2P lending marketplace. As per Goldman Sach estimate, 20% of bank lending will move to alternative finance, costing 12 billion dollar in profit loss for the bank. This is 7% of total profits for the banking sector.

Over next few years, due to regulation burden, number of players in banking will reduce. More and more consolidation will happen in the industry due to shrinkage of profit margins. Industry have already started to search for solutions to sustain their retail locations with reducing operational expenses and innovating to compete with startups in term of products & services. Though they have an edge in term of resources, corporate culture makes it difficult to innovate.

It a race between Innovation vs distribution as beautifully written by Alex Rampell .Will FinTech startups be able to get the distribution first or banks will be able to innovate first ? Race is ON.

Every week, a new startup is born to grab the 600 Billion remittance market volume . With an average fee of 7% approximately 40 billion dollar are paid in fees and despite dozens of startups trying to reduce it, fees are not coming down as anticipated. Even though we blame the remittance companies for higher fees, the industry have some additional challenges which other industries haven’t even heard of.

The biggest challenge in running a MSB ( Money Transfer Business ) isn’t higher cost of acquisition, technical debt, marketing but a Bank account. All MSBs are consideredHigh Risk Accounts (HRA)irrespective of size. It started with the Operation Choke Point which was announced in 2013 by United States Department of Justice. Every bank which is doing business with high risk clients such as payment processors, payday lenders, cheque cashing business & money service businesses are being investigated under this operation. Things have gone worse since then and accounts are being shut down. “De-Risking” is the common term used while closing a bank account. Banks are not interested in dealing with the MSB due to redflags that are raised both internally and externally in terms of compliance.

Maintaining a bank account is the biggest struggle in a money remittance business

Banks are justified on their end since in some cases, the cost associated with enhanced due diligence outweighs the cost of maintaining certain accounts. In other cases, banks mitigate the problem by charging premium fees to certain types of customers. This issue is not just limited to agents but the company itself. Here is an excerpt of World Bank survey report.

“A Significant portion of MTOs declared that the MTO principal (28% of the respondents) or its agents (45% of respondents) can no longer access banking services. Of that smaller group of MTO principals without access, 75% are maintaining their presence in the market by using alternative channels to clear and settle the amounts at international level; the other 25% of MTO principal respondents are currently unable to operate regularly through bank channels.”

Issue is that even though a MSB is 100% compliant, their account could be shut down without any reason. Regulators are well aware of the issues, however, none of them are super interested in solving this issue because there is no incentive. It is a continuos battle between the bank, MSB and regulator with no clear winner.

As per WorldBank recent report, 69% of the MSB are impacted due to recent account closures.

A bill should be passed by the assembly that as long as the business comply with the regulations, banking services shouldn’t be denied because it leads to either shutting down the business or using alternative underground routes such as Hawala. Bank account for a legally operated business should be a RIGHT. As an example; In Canada, even though basic banking services is a right for individual. Unfortunately, same rule doesn’t apply to businesses.

So next time, when some one plan to get into this industry, they should consider banking issue as the biggest hurdle, rather than the UI, logo or branding